Crypto exchanges aren’t doing so great at the moment. The latest on FTX, Gemini crypto exchange email leak, Binance might money laundering charges and defunct crypto exchange Quadriga sees bitcoin from wallets thought to be held by its supposedly ‘dead’ founder move for the first time since 2018…. The original PayPal founders say it has basically made itself into an episode of Black Mirror for its ‘totalitarian’ policies, Visa wants to allow auto bill payments from crypto wallets. Donald Trump released NFTs of himself, allegedly buying 1000 of them, himself. And the UN is piloting blockchain to get aid to people in Ukraine.

Table of Contents

- UN pilots blockchain-based system for getting aid to people in Ukraine

- Silvergate Capital Slapped With Lawsuit Over Ties With FTX And Alameda

- SEC was ‘asleep at the wheel’ about FTX

- Realised losses from FTX collapse peaked at $9B, far below earlier crises

- FTX ex-staffer: Extravagant expenditures and cult-like worshipping of SBF

- Sam Bankman-Fried seeks to reverse decision on contesting extradition

- FTX warns it will claw back political donations and contributions

- 350 new ‘scam tokens’ were created every day this year

- Should crypto projects ever negotiate with hackers? Probably

- Binance Proof-of-Reserves Auditor Mazars Pauses All Work for Crypto Clients

- Global Drug Conspiracy Used Binance To Launder Millions In Crypto, DEA Finds

- Binance and CEO Facing Possible Money Laundering Charges

- PayPal partners with ConsenSys MetaMask to allow US users to buy Ethereum

- PayPal has become an episode of Black Mirror

- $1.7M in Bitcoin tied to QuadrigaCX reawakens after years of dormancy

- BlockFi files motion to return frozen crypto to wallet users

- Microsoft Bans Crypto Mining on Its Online Services Without Permission

- Visa dreams up plans to let you auto-pay bills from your crypto wallet

- Amber Group acquires cryptocurrency platform Sparrow exchange

- OneCoin Co-Founder Karl Greenwood Pleads Guilty to Wire Fraud

- Metaverse experience to sway real-world travel choices in 2023

- Donald Trump releases NFTs of stock photos, skyrocket in value but still mocked

UN pilots blockchain-based system for getting aid to people in Ukraine

The United Nations Refugee Agency is piloting using blockchain to get digital cash payments to internally displaced people in Ukraine. The UNHCR is using the Stellar Development Foundation’s blockchain network for the aid-disbursement tool. Once it has confirmed the eligibility of an aid recipient, funds will be distributed in the USDC stablecoin. Recipients will have to download to a smartphone a digital wallet called Vibrant. Read More: UN pilots blockchain-based system for getting aid to people in Ukraine

Silvergate Capital Slapped With Lawsuit Over Ties With FTX And Alameda

California-based Silvergate Capital, the parent company of Silvergate Bank is now facing a class-action suit [PDF] for its connection with FTX alongside its CEO Alan Lane and Silvergate Bank. The lawsuit, filed in the California Southern District Court, accuses the bank of keeping FTX users’ deposits in Alameda’s bank accounts and claims Silvergate aided FTX’s fraudulent actions. U.S. senators have also queried Silvergate on its involvement with the exchange and lawmakers have asked Silvergate to explain where the customer funds went.

SEC was ‘asleep at the wheel’ about FTX

Texas Congressman Representative Pete Sessions has said the US SEC was “asleep at the wheel for these billions of dollars that we now find out about a year later” regarding how FTX Group and its subsidiaries met financial and corporate control requirements. “We need to look at what the Securities and Exchange Commission was doing”, he stated. He also noted that former FTX CEO Sam Bankman-Fried had “full access to members of Congress and the U.S. Senate.

Realised losses from FTX collapse peaked at $9B, far below earlier crises

Blockchain analytics firm Chainalysis has compared the peak weekly-realised losses after this year’s biggest crypto collapses in an attempt to put the FTX collapse into perspective.

Its report found the May depegging of Terra USD (UST) saw weekly-realised losses peak at $20.5 billion, while June’s collapses of Three Arrows Capital and Celsius saw them peak at $33 billion. FTX, by comparison, saw these losses peak at $9 billion in the week starting Nov. 7, and reducing weekly since. Read More: FTX Investor Impact: Timeline of Realized Cryptocurrency Gains and Losses Shows FTX Hit Investor Wallets Less Than Previous Crises

FTX ex-staffer: Extravagant expenditures and cult-like worshipping of SBF

A former FTX employee has shared details of what she describes as the crypto exchange’s ‘excessive luxury expenditures, obsessive workplace culture and grueling work hours that led to the hiring of a company psychiatrist in the year before its collapse’. Dani Cloud claimed time off from work to be a “joke” adding that “The work week was Monday to Sunday” and that a coworker was “chewed out” for asking if the company had time off for Thanksgiving. Of the company, she said “The entire operation was iconically and moronically inefficient”. Cloud said “I never knew all the things money could buy” claiming “FTX either purchased or rented multimillion-dollar homes for its executives, who threw lavish house parties and had private chefs”.

Sam Bankman-Fried seeks to reverse decision on contesting extradition

Sam Bankman-Fried, former FTX CEO, is now reportedly expected to appear in court in the Bahamas on Dec. 19 to consent to extradition to the USA, a reversal in his former decision to try and stay in the Bahamas. By consenting to extradition, he would instead appear in a United States court. This follows SBF being denied bail on Dec. 13 due to the “risk of flight.” He’s currently being held in the Bahamas’ only prison, Fox Hill, where conditions are reportedly “harsh” and overcrowded, with poor sanitation and nutrition and where detainees are alleged to have been physically abused by correctional officers. Read More: Exclusive: Sam Bankman-Fried to reverse decision on contesting extradition

FTX warns it will claw back political donations and contributions

The new management of FTX says it is now considering using legal avenues to recover the payments and contributions handed out by its former team. This could including the millions of dollars of political donations made by former CEO SBF. FTX says it had already “been approached by a number of recipients of contributions or other payments” that were made by, or at the direction of SBF or other officers, adding those entities have sought “directions for the return of such funds.” Last week, three prominent Democratic organisations reportedly pledged to return over $1 million. Read More: FTX Debtors Announce Process for Voluntary Return of Avoidable Payments

350 new ‘scam tokens’ were created every day this year

Over 350 scam crypto tokens were created per day in 2022. 1st Jan – 1st Dec 2022 saw a total of 117,629 “scam tokens” deployed, an 41% increase from 2021. The report by blockchain risk monitoring firm Solidus Labs cited the BNB Chain as harbouring the greatest number of scam tokens. It claims 12% of all BEP-20 tokens are scams followed by 8% built on Ethereum. Almost 2 million investors have lost money to rug pulls since Sep. 2020. This compared to the 1.8 million combined creditors affected by the bankruptcies of crypto exchanges and lending platforms FTX, Celsius, and Voyager. The most popular type of scam token this year was a “honeypot” – a token smart contract that doesn’t allow buyers to resell. The most prolific “honeypot” in 2022 was the $3.3 million Squid Game (SQUID) token scam which grew 45,000% in a few days before anonymous founders apparently ran off with investor funds. Read More: The 2022 Rug Pull Report [PDF]

Should crypto projects ever negotiate with hackers? Probably

Should you call the law enforcement about DeFi exploits? Not necessarily immediately, experts claim. How to fix DeFi vulnerabilities? And is there anything you can do to outsmart hackers? Not as much as you might like. Read More: Features Should crypto projects ever negotiate with hackers? Probably

Binance Proof-of-Reserves Auditor Mazars Pauses All Work for Crypto Clients

Auditing firm Mazars has reportedly paused all work for crypto clients relating to proof-of-reserves reports. “This is due to concerns regarding the way these reports are understood by the public” a Mazers statement said. Mazers’ clients include Binance, Crypto .com, and KuCoin. Mazars has reportedly deleted Binance’s proof-of-reserves assessment, which allegedly found its bitcoin reserves were over-collateralised. Binance’s BNB coin fell about 5% in the 24 hours following the announcement. Some lawyers have commented that this doesn’t shout out good news for Binance. Read More: Binance Proof-of-Reserves Auditor Mazars Pauses All Work for Crypto Clients

Global Drug Conspiracy Used Binance To Launder Millions In Crypto, DEA Finds

A Mexican methamphetamine and cocaine gang operating across the U.S., Mexico, Europe and Australia reportedly used crypto exchange Binance to launder tens of millions in drug proceeds, according to an ongoing investigation by the US Drug Enforcement Administration (DEA). It’s thought that between $15 and $40 million in illicit proceeds might have allegedly been funnelled through Binance. Te investigation into the gang’s use of Binance began in 2020, when peer to peer exchange localbitcoins was initially used to exchange crypto for cash. Binance has been helping the DEA to trace the funds and identity the account owners. Binance senior director of investigations Matthew Price, a former IRS cybercrime agent said “This is actually an example of where the transparency of blockchain transactions works against criminal actors,” Price told Forbes. “The bad guys are leaving a permanent record of what they’re doing. This, after Binance CEO CZ may face potential money laundering charges. Read More: Global Drug Conspiracy Used Binance To Launder Millions In Crypto, DEA Investigation Finds

Binance and CEO Facing Possible Money Laundering Charges

U.S. prosecutors may reportedly charge Binance and its top executives including CEO CZ with money laundering and sanctions violations. This is the latest in a probe that began in 2018 which hasn’t been helped by the collapse of fellow crypto exchange FTX. It’s been reported that Department of Justice officials are split, however, about whether to proceed, with some wanting more time to review evidence. Read More: Binance CEO Facing Possible Money Laundering Charges

PayPal partners with ConsenSys MetaMask to allow US users to buy Ethereum

US users of self-custodial wallet MetaMask will now be able to purchase Ethereum from within the app using PayPal. PayPal being the company now notorious for wanting to freeze customer accounts and which has reinstated what some see as a tyrannical policy charge on customer accounts for $2500 for posts it doesn’t like on social media. MetaMask is so far the only Web 3.0 wallet to utilise PayPal to increase on-ramp transactions. Read More:

- PayPal partners with ConsenSys MetaMask to allow US users to buy Ethereum

- PayPal Brings Back $2500 Penalty for Violations of Acceptable Use Policy

Update: PayPal has quietly removed the $2500 penalty for transgressions of their Acceptable Use Policy. The most recent update indicates October 29, 2022.

PayPal has become an episode of Black Mirror

The early founders of PayPal including Peter Thiel and Elon Musk dubbed the “PayPal Mafia,” have slammed PayPal over its new debanking policies they consider to be “totalitarian”. PayPal has caught a lot of negative headlines over its de-platforming practices, which reportedly involve abruptly freezing users’ funds, fines and ‘frosty negotiations to unlock the accounts of its users’. Peter Thiel, who co-founded PayPal in 1998 and served as its CEO until 2002, said of the platform now: “If the online forms of your money are frozen, that’s like destroying people economically, limiting their ability to exercise their political voice,” adding that: “There’s something about destroying people economically that seems like a far more totalitarian thing.” This isn’t about crypto. But just goes to highlight the danger to freedom and human rights brought by relying on centralised payment institutions, and CBDCs, that can block your funds at any time. Read More:

- PayPal seizes alternative media site’s money

- What the Hell Happened to PayPal?

$1.7M in Bitcoin tied to QuadrigaCX reawakens after years of dormancy

Five wallets tied to the now defunct Canadian crypto exchange QuadrigaCX have just moved around 104 Bitcoin worth $1.7 million. The five wallets in question were thought to be inaccessible following the supposed death of Gerald Cotten, the exchange’s founder and CEO, in December 2018, as he had sole responsibility for the wallet’s private keys. This is the first time movement has been seen from these wallets since at least April 2018. QuadrigaCX had been Canada’s largest crypto exchange until it declared bankruptcy in April 2019 following Cotten’s death, when it was revealed the exchange had operated like a Ponzi scheme with users losing their funds. This led to theories that he faked his own death as part of a fraudulent exit scam. I have yet to meet anyone in crypto who actually believes he died. This could be interesting….

BlockFi files motion to return frozen crypto to wallet users

BlockFi has filed a motion to ask for authority from the United States Bankruptcy Court to allow its users to withdraw digital assets currently locked up in BlockFi Wallets. The bankrupt crypto lending platform called the motion an “important step toward our goal of returning assets to clients through our chapter 11 cases,” adding “It is our belief that clients unambiguously own the digital assets in their BlockFi Wallet Accounts.”

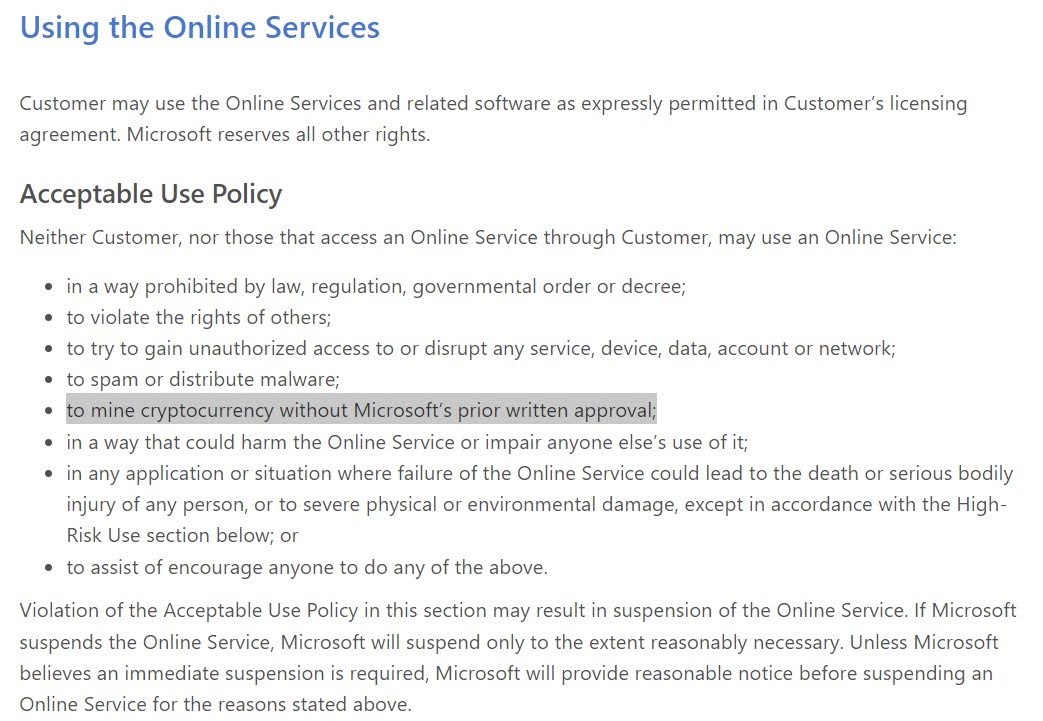

Microsoft Bans Crypto Mining on Its Online Services Without Permission

Microsoft has banned customers from doing crypto mining on its online services without getting prior permission, which it’s fair to guess they’re not going to rush to grant. Microsoft’s update said “Neither Customer, nor those that access an Online Service through Customer, may use an Online Service … to mine cryptocurrency without Microsoft’s prior written approval”. Microsoft isn’t the only tech company to put such a policy in place. Google has a similar policy and Amazon’s AWS prohibits crypto mining during its 12-month free trial. Google has said most of the “malicious actors” have used compromised cloud accounts to mine crypto.

Neither Customer, nor those that access an Online Service through Customer, may use an Online Service: to mine cryptocurrency without Microsoft’s prior written approval; – Microsoft Licensing For Online Services

The Acceptable Use Policy has been updated to explicitly prohibit mining for cryptocurrencies across all Microsoft Online Services unless written pre-approval is granted by Microsoft. – Important actions partners need to take to secure the partner ecosystem

You may not use AWS Services under any Offers to mine for cryptocurrency. If you use AWS Services under an Offer to mine for cryptocurrency, we may charge you standard rates for your use of the AWS Services, and we may suspend your right to access or use any portion or all of the Service Offerings. – AWS Free Tier Terms

3.3 Restrictions. Customer will not, and will not allow End Users to, (a) copy, modify, or create a derivative work of the Services; (b) reverse engineer, decompile, translate, disassemble, or otherwise attempt to extract any or all of the source code of, the Services (except to the extent such restriction is expressly prohibited by applicable law); (c) sell, resell, sublicense, transfer, or distribute any or all of the Services; or (d) access or use the Services (i) for High Risk Activities; (ii) in violation of the AUP; (iii) in a manner intended to avoid incurring Fees (including creating multiple Customer Applications, Accounts, or Projects to simulate or act as a single Customer Application, Account, or Project (respectively)) or to circumvent Service-specific usage limits or quotas; (iv) to engage in cryptocurrency mining without Google’s prior written approval; (v) to operate or enable any telecommunications service or in connection with any Customer Application that allows End Users to place calls or to receive calls from any public switched telephone network, unless otherwise described in the Service Specific Terms; (vi) for materials or activities that are subject to the International Traffic in Arms Regulations (ITAR) maintained by the United States Department of State; (vii) in a manner that breaches, or causes the breach of, Export Control Laws; or (viii) to transmit, store, or process health information subject to United States HIPAA regulations except as permitted by an executed HIPAA BAA. – Google Cloud Platform Terms of Service

Visa dreams up plans to let you auto-pay bills from your crypto wallet

Visa has claimed that crypto users may one day be able to automatically pay their electricity and telephone bills through their self-custodial crypto wallets. Its crypto thought leadership team proposed a way that would allow providers to automatically “pull” funds from users’ Ethereum-powered crypto wallets, without requiring users to manually sign off on every transaction. Direct debit type automated payments aren’t currently possible through self custody wallets as the user is the only person in control of the private keys, meaning they need to manually sign off on transactions as “a smart contract cannot initiate transactions on its own.” Read More: Exploring new avenues of blockchain innovation

Amber Group acquires cryptocurrency platform Sparrow exchange

Amber Group, a cryptocurrency trading firm has reportedly acquired Singaporean crypto platform Sparrow Holdings, which offers digital assets products and solutions. This after recent layoffs bringing the group’s headcount to less than 400 from a peak of 1,100. Read More: Amber Group Acquires Singapore Crypto Exchange

OneCoin Co-Founder Karl Greenwood Pleads Guilty to Wire Fraud

Karl Greenwood, the Co-Founder of multi-billion dollar Ponzi scheme OneCoin, has pleaded guilty to charges of wire fraud and money laundering in connection with his role in the project. He faces a maximum of 20 or 60 years in prison (depending on which source you trust) and is to be sentenced on April 5, 2023. Read More: Co-Founder Of Multi-Billion-Dollar Cryptocurrency Pyramid Scheme “OneCoin” Pleads Guilty

Metaverse experience to sway real-world travel choices in 2023

A survey of 24,179 respondents across 32 countries found that 43% intend to use virtual reality to inspire their travel choices. Those most likely to try out travel experiences in the metaverse were Gen Z (1997-2012) (45%) and Millennials (1981-1996) (43%). Over 35% said they were open to spending multiple days in the Metaverse to get the hang of the surroundings of popular destinations, whereas 60% believe that the experiences the Metaverse and virtual technologies offer don’t come close to in-person experiences. Read More: Travel Predictions 2023

Donald Trump releases NFTs of stock photos, skyrocket in value but still mocked

Donald Trump, who has previously criticised all things crypto, has used the technology it’s built on to launch his own collection of NFT trading cards. The NFTs sold out within hours and surged hugely from their initial sale price of $99, with the floor price still in the hundreds of dollars. This, despite accusations that the team behind the NFTs used stock images from Shutterstock and allegedly left the Shutterstock watermarks on the NFT photos. Nothing like spending hundreds of dollars to own a copy of a photo of Donald Trump. The largest user owns approximately 1,000 of the NFT cards and is claimed by some to be Donald Trump himself. This bears similarities to Melania Trump’s NFT release, which is alleged to have been bought by…. Melania herself… Read More: Donald Trump Trading Card NFTs Skyrocket in Value Despite Being Mocked for His ‘Major Announcement’